Tally CEO: Automation is the key to democratizing consumer finance

Jason Brown shares his 20-year forecast at the 2018 Fintech Inclusion Summit Tally CEO and Co-founder Jason Brown headlined the 2018 Fintech Inclusion Summit in San Francisco on Oct. 29 with a thought-provoking keynote address on the future of consumer […]

Gregory Andersen

Managing Editor at Tally

November 5, 2018

Jason Brown shares his 20-year forecast at the 2018 Fintech Inclusion Summit

Tally CEO and Co-founder Jason Brown headlined the 2018 Fintech Inclusion Summit in San Francisco on Oct. 29 with a thought-provoking keynote address on the future of consumer finance and the pivotal role that automation plays.

Hosted by Fintech Devs & PMs, the summit featured a slate of presentations and discussions with founders, investors, business leaders and product managers in the booming fintech industry, including CFSi, Affirm, 500 Startups and Gusto.

Brown delved into Tally’s origin story and told an audience of about 200 people at the Golden Gate Club in the Presidio how the business was formed and the early lessons he learned.

“We decided to start with credit card debt because it’s one of the hardest, most widespread financial problems to solve for Americans. And on that foundation, we would then automate the rest of it.”

Brown and his team discovered that, to achieve full automation, Tally would have to start from scratch and use Scala microservices to build an entire bank core from the ledger up.

“We thought it would take us a year,” he said. “It took us three.”

They needed to have the full ability to use algorithms to underwrite customers, transmit and lend money, and do all of the necessary financial work that enables Tally to provide its customers with a work-free experience.

“Even getting customers to click buttons and fill out forms — that’s a tall order, and that causes people not to get the benefits of products,” Brown said. “So, you have to engineer around all of that, so that customers can just sit back and let you do the work for them.”

When you think of most consumer finance apps, Brown said, you think of charts, graphs and recommendations about how to manage your money. But Tally has taken an entirely different approach, which is why Tally’s home screen features a person enjoying a cup of coffee with their feet on the table.

The imagery is intended to convey a sense of relief — that Tally is handling the hard work behind the scenes while the customer kicks back and relaxes.

“Our view is that, in the future, you will have a completely invisible and ambient service that will mediate your entire financial life on your behalf,” Brown said.

Rex Salisbury, founder of Fintech Devs & PMs, echoed the importance of automation in minimizing how hard a user must work to get the benefit of a product.

“I’m very excited about the prospect of automating aspects of consumers' financials lives. I also appreciate that Tally has done the hard work that automation requires,” Salisbury said. “Automation isn't something that just happens. Automation is about deep, painful integration against the long tail of financial service providers to make sure that the most a user ever needs to do is click a button — and sometimes not even that.”

Tally's home screen may seem pretty chill — a person with their feet up, drinking a cup of coffee — but behind the scenes, Tally is doing all the hard work on a user's behalf.

How Tally is different from the rest of consumer finance

What’s unique about Tally is that it separates the burden of credit cards from the benefit. Brown explained that customers still use their credit cards to get all of the points and rewards that come with them.

Nothing changes in the way people spend. Tally simply sweeps over the customers’ balances a few times per week, if the banks are charging them interest, and moves their balances to Tally’s ledger. Tally still charges customers interest, according to Brown, but substantially less than what the banks charge.

Beyond the interest savings, Brown boasted about Tally’s ability to prevent against late fees. Sixteen percent of Americans use autopay for credit cards, he said, which means the average person is making 48 manual payments per year and, collectively, the United States is spending about $12 billion in late fees.

“They use [autopay] for other fixed payments, like student loans or rent,” he said. “But with credit cards, it varies, and people are concerned it's going to lead to overdrafting.”

“I’m very excited about the prospect of automating aspects of consumers' financials lives. I also appreciate that Tally has done the hard work that automation requires.”— Rex Salisbury, founder of Fintech Devs & PMs

But the biggest advantage of Tally, according to Brown, is how the company uses algorithms to manage customers’ debt and get them out of debt faster.

“That’s the No. 1 thing someone with credit card needs to do: get out of credit card debt,” he said.

Tally Advisor, the app’s newest feature, works toward that very objective. Brown described it as a “robo-advisor for credit card debt.” Tally takes into account a customer’s income, spending and total debt, then helps them set a realistic date to become debt-free.

And it’s working: Brown said, on average, customers are getting out credit card debt 10 to 15 years faster.

Tally found 52 percent of people with an “excellent” credit score experience anxiety about their credit cards, compared 67 percent of those with a “good” credit score.

A new way to improve the lives of others

At the time of Tally’s inception, the primary goal was exactly what they’re doing now: getting people out from underneath their debt as fast as possible.

But Brown said the company’s trajectory dramatically changed when he and Jasper Platz, Tally’s president and co-founder, began digging into another aspect of credit card debt.

“The big eye-opener for us was when we realized it’s not about money,” Brown said.

Tally conducted surveys to understand the emotions that people who have credit card debt are experiencing. Brown initially believed the primary emotion would be regret or sadness, but learned anxiety is the most common feeling among this segment of the population.

“Anxiety is actually a fear emotion,” he said. “It’s the sense that there’s an unknown threat in the future, or out there somewhere, that you don’t have the tools to counteract and protect yourself. It’s a fear feeling that you don’t have the tools necessary to change your outcome.”

Brown discovered the true power of automation is, first and foremost, actually freeing people from the emotional burden of credit card debt. Ultimately, this realization helped Tally focus its mission of helping people become less stressed and better off financially.

Fintech companies have been able to focus on individual things that banks traditionally offered and do them in a better way, but Tally is the only one with its sights set on credit card debt.

How can fintech compete with big banks?

The financial crisis in 2008 fundamentally rocked consumers’ faith in the way they viewed the banking industry.

Brown believes that created an opportunity for these fintech companies to come in an effectively “unbundle” the banks. That is, it allowed newcomers to focus on one or two things a bank traditionally offered and do it in a better way.

But with the inherent advantages of scale and distribution, Brown said, the banks are now catching up. They’re able to sit back and hand-select the best and brightest ideas emerging from the fintech industry and provide a watered-down version of that idea to their customers.

“Because the core bank account is so sticky,” he said, “they end up retaining those customers.”

In Brown’s estimation, there’s only one way to remain competitive in the consumer finance space: automation.

“The No. 1 thing banks do not want to have happen is to have fintech own this relationship and turn them into pipes,” he said. “They don’t want to be a utility. Because if they are a utility, that means all the excess rents they’re earning through all their products get compressed, and most of those get returned to the customer. And they lose the ownership of the customer.”

“Our view is that, in the future, you will have a completely invisible and ambient service that will mediate your entire financial life on your behalf.” — Jason Brown, Tally CEO and Co-founder

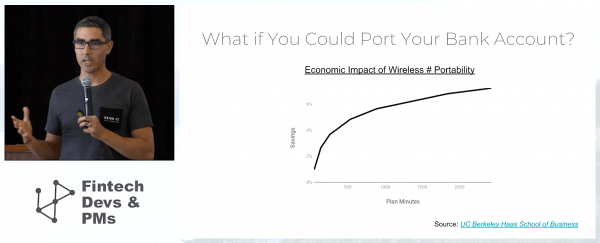

Brown used the example of cellphone number portability to explain the big banks’ ability to retain customers. Prior to 2003, people who wanted to change cellphone service providers typically had to forfeit their phone numbers, and fear of losing their phone numbers prompted many customers to remain with their service providers.

“If there’s friction in switching providers, from any service to another, it always benefits the incumbents,” Brown said. “It allows the incumbents to charge excess rents that would otherwise not be there.”

But once the government stepped in and forced these companies to allow people to port their cellphone numbers from one service provider to another, that friction was reduced, and customers immediately saw savings on their monthly bills. As time went on, and these companies had to work harder to retain customers by providing better services and charging less.

In that sense, according to Brown, automation is the ultimate reduction in friction.

When cellphone service providers were ordered to allow customers to port their phone numbers from one company to another, the average customer’s savings immediately increased. Now, imagine the savings if bank accounts were portable.

Automation is the great equalizer

Using automation to reduce friction is how the fintech industry can create more inclusive products because, right now, only the ultra-wealthy have 100 percent automation. They have the means to hire people numerous people to do all of their financial work for them.

“If we can collectively build automated services that can democratize that, so that every normal person can have what the ultra-wealthy have now, we’ll be living in the future,” Brown said.

A fully automated product, Brown said, ensures that customers don’t have to carry the cognitive load, invest their time or spend money to move their financial profile from one place to another. And the ability to do so — removing the current “stickiness” of financial institutions — is why automation is poised to be the great equalizer.

“I think Jason hit the nail on the head,” Salisbury said following Brown’s keynote address. “The only way to deliver real value for people is to focus on doing the work for people. Rich people already have this because they can hire humans. The only way the rest of us will get access to a similar level of services is with access to something with a lower marginal cost than human labor.”

So, what's next for consumer finance?

“The next 20 years are going to be defined by taking the cognitive load off of people’s plates, so to speak, and doing it all for them,” Brown said. “We will be giving people back time, but I think what’s more important is that we will be giving people back a positive emotional state. It will be, conceptually, taking this anxiety that's on their shoulders and putting on the shoulders of machines. And, suddenly, they won’t know any better because that's just the way it will have always been. But we will be taking burden off of people's lives and erasing that from the human experience.”