What is APR? Credit card interest rates explained

Credit card APR is a key part in choosing the right card for you.

Justin Cupler

Contributing Writer at Tally

August 18, 2020

When applying for a credit card, you get a lot of numbers thrown your way, including credit limit, rewards points, annual fees and APR. They’re all worth considering, but APR is especially important because it impacts your minimum payments and how long it will take you to pay off a credit card balance.

To help you understand credit card APR, we'll cover the various types of APR, how it’s calculated and how to avoid paying it. Let’s start with the basics and explore what credit card APR is and how it's different from other types of APR.

What is APR? Credit card interest explained

Credit card annual percentage rate (APR) is the amount your credit card charges on the balance you owe. Credit card APR is expressed as a percentage that’s also known as the interest rate.

Credit cards can have a fixed APR or a variable APR.

A fixed APR means the APR on your credit card is unchanged once you accept the terms. (The one exception is if you encounter a penalty fee.)

A variable APR means the APR on your credit card can increase or decrease. You start with a base rate, and changes to your APRs usually correspond with the increases and decreases in an index rate.

Most credit card companies use the Prime Rate, which is the interest rate reported by the Wall Street Journal via a survey of the 30 largest banks in the U.S.

Credit card APR vs. loan APR

The APR on loans, like on mortgages and personal loans, isn’t the same as credit card APR.

For loans, the APR includes the interest rate, but it also includes the fees the lender rolled into the loan, like closing costs and origination fees. This is why you often see both an interest rate and an APR when applying for a loan. The APR on a loan is often higher than the interest rate.

On a credit card, you’ll only see the APR, which is the same as the interest rate.

How your credit card APR is determined

Credit card companies determine your APR using several variables, and the process varies for fixed APR and variable APR credit cards.

Fixed-rate credit card

A fixed APR credit card starts with the index rate. The credit card company then applies its margin, which is the number of percentage points it adds to the index rate. The result is your base rate.

For example, if the index rate is 3.25%, and your credit card company has an 18-percentage-point margin, your base APR would be 21.25%.

Using the base APR, the credit card company creates its APR range or APR tiers. An example of an APR range would be 21.25% to 29.25%. An example of APR tiers would be 21.25%, 23.25%, 27.25% or 29.25%.

The APR you receive from the credit card issuer depends on your creditworthiness, but it will be within their APR range or one of their tiers.

If you have excellent credit, you will likely get a lower APR. With a fair or bad credit score, you'll likely end up with a higher APR.

Variable-rate credit card

A variable APR card also uses an index rate, but your APR is expressed as index rate + margin. With variable APR, the margin is determined by your creditworthiness — the higher your credit score, the lower the margin.

For example, with excellent credit, you may receive an index rate + 13.75% variable APR. But if you have average credit, you may receive an index rate + 15.5% variable APR.

Types of credit card APR

Credit cards often have different APRs for various situations, including:

Purchase APR

This is the APR assigned to everyday purchases. It’s also the most prominent APR presented to you when applying for a credit card and accepting the credit card terms.

Promotional APR

Promotional APR is a lower interest rate the credit card company charges you on all purchases in special circumstances, like during the first few months as a new cardholder or around a holiday. An introductory rate is a common example of a promotional APR.

Traditional credit cards generally only offer promotional APR for a limited time, such as 1.9% APR for six months.

Store credit cards often offer ongoing promotional APR on in-store purchases of a certain amount, like 0% APR for 12 months on in-store purchases over $500.

Deferred APR

Store credit cards also offer deferred APR promotions, like deferred interest for 12 months on in-store purchases over $500.

These APR offers don't apply interest to your account during the promotional period. However, if you fail to pay off the balance within the promotional period, the credit card company will retroactively apply interest charges to any unpaid balance.

So, if you charge $1,000 on a credit card with a 12-month deferred interest promotion and pay off $900 of it within the promotion period, the credit card company will retroactively apply the past 12 months of deferred APR to the remaining $100 balance.

Balance transfer APR

Balance transfer APR allows cardholders to transfer balances from a higher-interest credit card to a new credit card at a lower rate for a specified period. Balance transfer APR terms vary greatly by card, but they are generally 0% APR for 12-18 months and require a 3% to 4% balance transfer fee.

Unlike deferred APR, the interest charges don't apply retroactively if you don't pay them off within the promotional period. Instead, they start accruing interest after the promotion's expiration.

Credit card companies offer low-interest balance transfers to attract new customers or entice existing cardholders to use their cards.

Cash advance APR

Many credit cards also offer the ability to go to an ATM and withdraw cash. This is called a cash advance.

Credit cards that offer this service also have a cash advance APR, which is generally a little higher than your purchase APR. Cash advances also sometimes include a fee.

Penalty APR

If you break the credit card terms, your credit card issuer may charge you a penalty APR. Breaking the terms can include making late payments, exceeding the credit limit or having any other unauthorized use of the credit card.

The penalty APR is typically significantly higher than your purchase APR and remains for a specified amount of time.

For example, if your purchase APR is 21.99%, your credit card company may have a 29.99% penalty APR.

Not all credit card companies apply penalty APRs, and they must provide you a 45-day written notice before applying the new APR, according to the CARD Act of 2009.

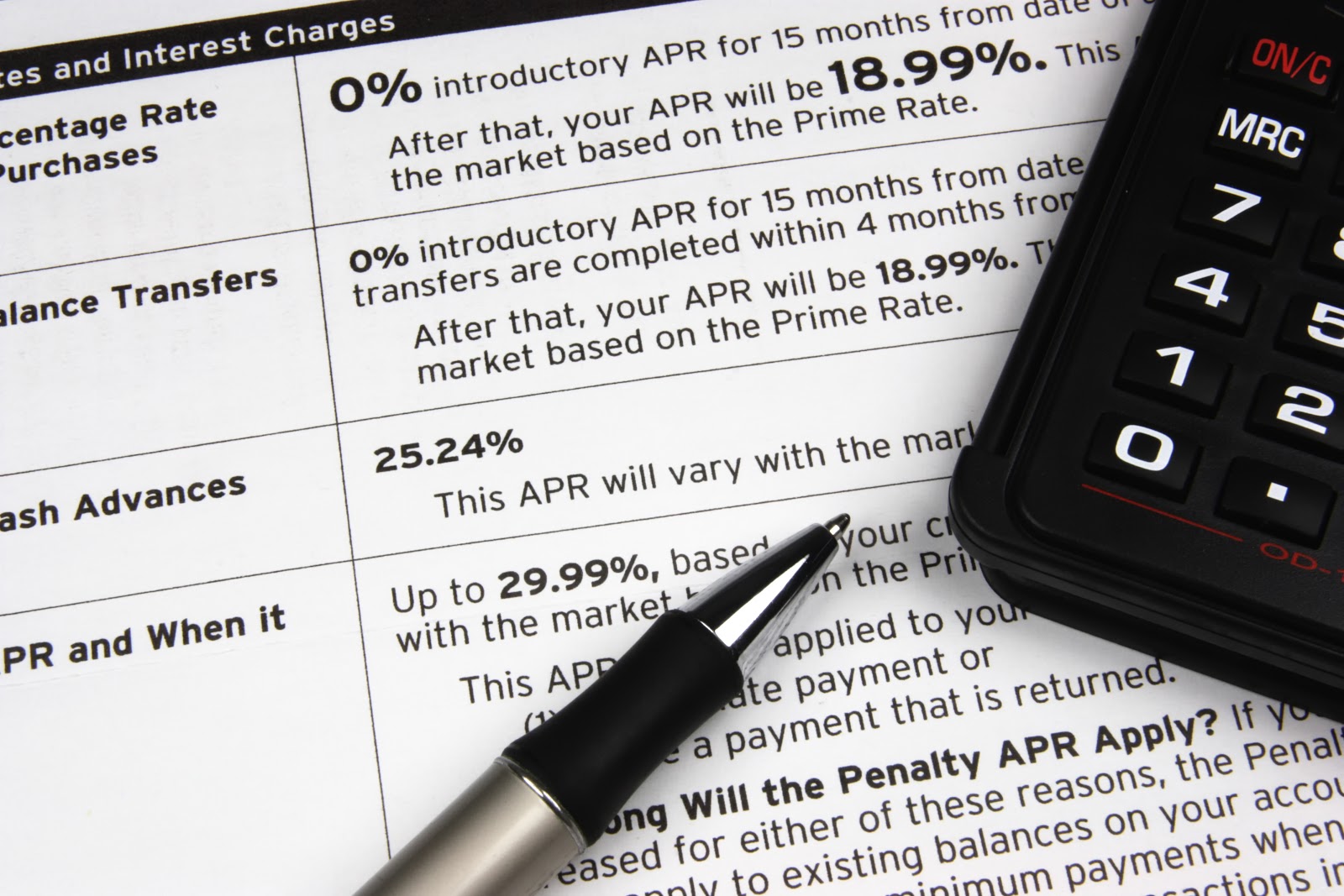

Finding your APR

You can find your credit card's APR on your monthly statement or in the credit card terms and conditions. It's in an area called the "Schumer box," named after Senator Chuck Schumer, who introduced legislation requiring credit card companies to disclose APR and other fees in all promotional materials.

The Schumer box includes all the key fees associated with your credit card:

Purchase APR

Variable APR terms (if applicable)

Balance transfer APR

Penalty APR

Cash advance APR

Annual fee

Balance transfer fees

Cash advance fees

Foreign transaction fees

Late payment fees

Returned check fees

If you don't receive paper credit card statements, you can find copies of your statements online or through your credit card's mobile app. It's usually under a tab or on a page named "Statements" or "Statements and Documents."

You can also find your credit card’s terms and conditions online or on your credit card’s mobile app under a section titled “Disclosures,” “Terms & Conditions” or something similar.

Credit card APR calculations

Credit card companies can calculate APR either daily or monthly. You can find out how your credit card calculates APR on your credit card terms and conditions. Below are a few examples of daily and monthly APR calculations:

Daily APR calculation

You can calculate daily APR in four steps.

Find the daily periodic rate by dividing the APR by 365 (the number of days in a year).

Example: If your credit card has 20% APR, the daily periodic rate is 0.05%

Formula: 0.20 ÷ 365 = 0.000547

Calculate your average daily balance. Add up your daily balance for each day in a billing cycle and divide the total by the number of days in the billing cycle.

If your balance changes every day, you must go through day by day and add together each day. If you make no new charges on your account for an entire billing cycle, the average daily balance remains the same all month.

Example: You start the month with a $100 balance and make no additional purchases for 20 days. If you make a new $100 purchase and carry a $200 balance for the last eight days of the billing cycle, your average daily balance will be $128.57

Formula: [(100 × 20) + (200 × 8)] ÷ 28 = 128.57

Multiply the average daily balance by the daily periodic rate to get the daily APR charges.

Example: If your average daily balance is $128.57 and your daily periodic rate is 0.05%, your daily APR charge would be 6.4 cents.

Formula: 128.57 × 0.05 = 0.064

Multiply the daily APR charge by the number of days in the billing cycle.

Example: If your daily APR charge is 6.4 cents and there are 28 days in the billing cycle, your monthly APR charge would be $1.80.

Formula: 0.064 × 28 = 1.80

Monthly APR calculation

You can calculate monthly APR in two steps.

Find your monthly periodic rate by dividing your APR by 12 (the number of months in a year).

Example: If you have a 20% APR credit card, the monthly periodic rate is 1.7%

Formula: 0.20 ÷ 12 = 0.01666

Multiply your credit card balance by the monthly periodic rate to get the monthly APR charges.

Example: If you have a $200 balance on your credit card, your monthly APR charge would be $3.40.

Formula: 200 × 1.7 = 3.40

Avoiding APR charges

Your credit card issuer will often give you a grace period, which is the time between the end of your billing cycle and your payment due date. During this time, you won't be charged interest on your account.

If you pay your balance in full by the due date, the credit card company will apply no interest charges to your account.

Not all credit card companies offer a grace period. Those that do generally offer it only on purchase APR. You can find out if your credit card offers a grace period in the Schumer box on your credit card terms and conditions.

Understanding APR can help you save

APR is one of the most important factors to consider when applying for a credit card. It can have a significant effect on how much money you pay in interest and how long it takes to pay off your balance.

When weighing your credit card options, make sure you know if your credit card APR has a fixed rate or a variable rate, and look at more than just the purchase APR. Also, make note of whether your credit card APR is calculated daily or monthly — you can even calculate it yourself with the formulas above.

Lastly, remember that you can avoid APR charges altogether if you pay your balance in full before the due date. If you can’t pay your entire balance, pay as much as you can now to avoid spending more money on interest in the long run.