Should I make the minimum payment on my credit card?

Paying more than the minimum can save you money on interest and get you out of debt faster.

Sarah Li Cain

Contributing Writer at Tally

May 22, 2019

Credit cards can give you the flexibility and convenience of spending money as you see fit and paying it back over time. Sometimes, it only takes a day or two. Other times, it can take weeks, months or even years to repay your credit card balance.

So when you receive your credit card statement every month, it’s tempting to only make the minimum payment. The amount can seem manageable, but it’s a temporary relief.

Only making the minimum payment on your credit cards will cost you big bucks over time.

Let’s explore why you’re better off paying off as much as you can afford on your credit cards every month.

You can save money on interest

Credit card companies want you to make the minimum payment. When you do, they make more money off you. That’s because the less you pay toward your balance each month, the more interest you rack up on your credit cards.

Riley Adams, a licensed CPA in Louisiana and founder of Young and the Invested, encourages people to pay off their credit card balance in full whenever possible.

“It usually makes sense because you’re not paying any interest,” Adams says. “At the very least, make more than the monthly minimum so you can pay as little [interest] to the credit card companies as possible.”

Are you wondering how much of a difference this will actually make? Put simply: Making more than the minimum payment on your credit cards could save you hundreds or even thousands of dollars in interest.

Let’s say you have a $3,000 credit card balance at 18% APR, and your minimum payment is $75 each month. If you only make the minimum payment, you’ll end up spending $3,923.20 in interest before you pay off your balance.

But if you bump up your monthly payment to $100 month, you’ll only pay $1,015.49 in interest — saving you $2,907.71. (Check out how much you can save by increasing your monthly payment.)

And that’s just one credit card balance. If you have multiple credit cards, consider how much you can save just by making more than the minimum payments.

You can get out of debt faster

Nobody wants to be in debt forever. Studies show the anxiety experienced by people dealing with credit card debt is proportional to the amount of debt they have. That means getting out of debt faster comes with added emotional benefits.

The sooner you pay off your credit cards, the better you’ll feel. Now, think about what else you could do with the money you’re currently putting toward your credit card balances — set it aside for an emergency fund, start a retirement account or get ahead on your mortgage payments.

Making more than the minimum payment on your credit card will help you get out of debt faster. We’re talking months, even years faster.

Again, let’s say you have a $3,000 credit card balance at 18% APR, and your minimum payment is $75 each month. If you only make the minimum payment, it will take you more than 18 years to pay off the entire balance. But if you increase your payment to $100 a month, it will take about 3 years to pay it off.

An extra $25 a month can get you out of debt nearly 15 years faster!

You can improve your credit score

Looking to qualify for a better mortgage rate? Want to increase your credit limit? Paying more than the minimum on your credit card balance will help you improve your credit score, too.

Courtney Nagle, an associate marketing manager at National Foundation for Credit Counseling, understands that people think that keeping a balance on your credit card will help.

“It’s a total myth that you need to keep a balance on your credit card to improve your score,” Nagle says.

In other words, paying off your credit card balance as soon as possible won’t hurt your credit score. In fact, it should improve it.

Paying off your balance will reduce your credit utilization rate, which is the amount of credit you’re using at any given time. The higher the rate — most experts say 30% is ideal — the more likely your credit score will go down.

A low credit score can make it difficult to get better rates or even approved for future loans. Your credit score can even affect your ability to secure housing because landlords take your credit history into consideration.

Paying more than the minimum on your credit card can decrease your overall balance faster and improve your credit utilization rate. It can also help minimize your debt, especially if you continue to use your credit card.

If you consistently make on-time payments toward your credit cards that are more than the minimum payment, you can ask for a credit limit increase. And that can lower your credit utilization rate even more.

Does it ever make sense to only make the minimum payment?

Yes, there’s always an exception to the rule.

As a general rule, you should get in the habit of making more than your minimum credit card payment. But there are some situations where it may make sense to pay only your minimum, temporarily.

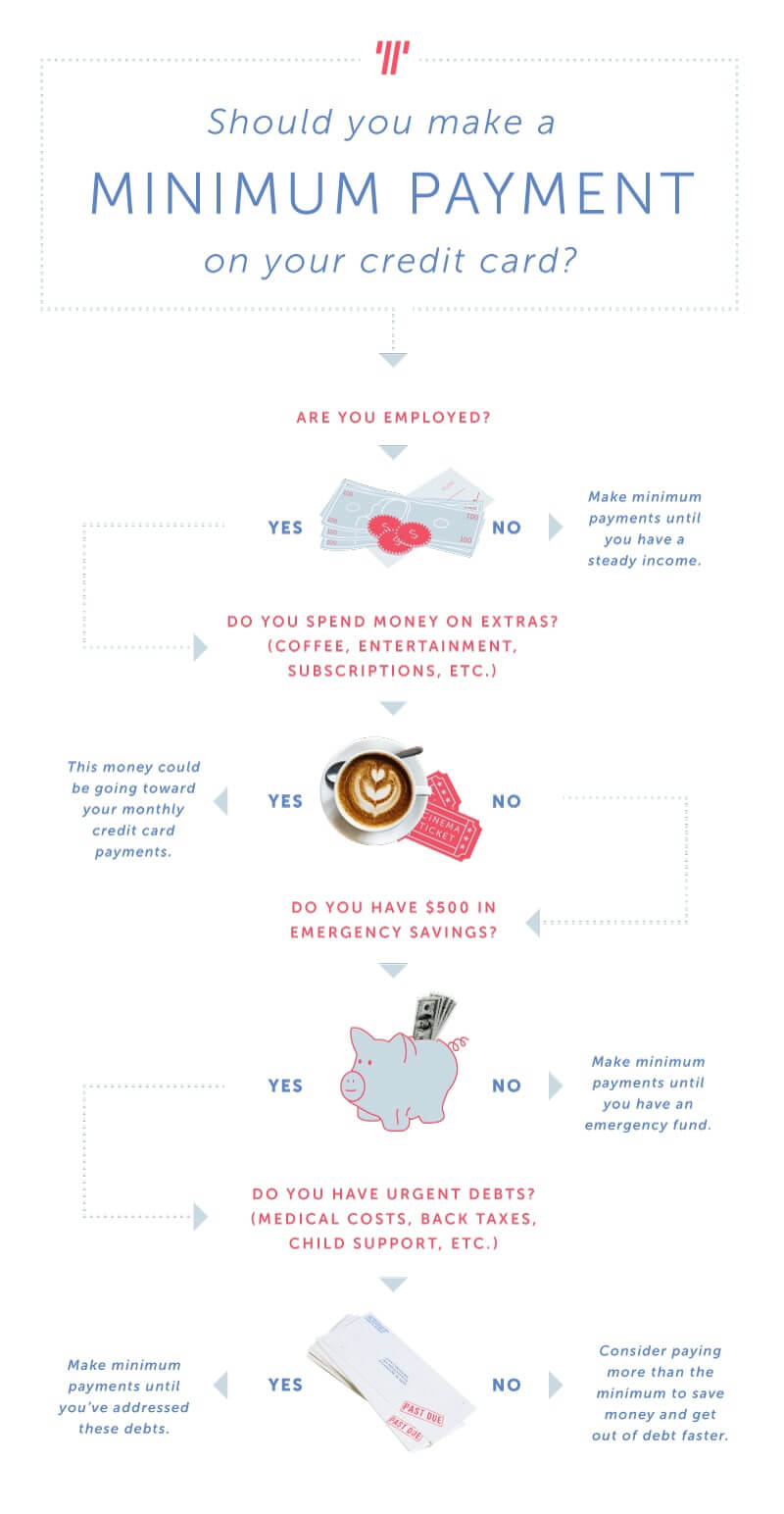

Wondering if you should make a minimum payment on your credit card? Ask yourself a few simple questions. (Illustration by Laura Jay/Tally)

Urgent debts: If you owe money to more than just the credit card companies, consider shifting your priorities. You may also want to only make the minimum payment on your credit cards if you have outstanding medical expenses, IRS payments, child support payments, alimony and other debts that carry significant penalties.

Upcoming expenses: If you know you’re going to dip into your pockets in the near future, it makes sense to start saving immediately. Making the minimum payments on your credit cards may allow you to start setting money aside in advance — and that could prevent you from going further into debt in the long run.

No emergency savings: Much like upcoming expenses, it’s important to set yourself up for success and protect yourself from hardship. Most financial experts say having $500 in emergency savings is more important than extra money toward your credit card balance. Without an emergency fund, you’ll likely need to use your credit card when unexpected costs come up, and that could put you in an even more difficult situation.

“Minimum payments can make sense for people in certain situations,” says Bethy Hardeman, a personal finance expert at Tally. “When life happens, we sometimes need to adjust our priorities. But only paying the minimum is not a long-term strategy. It’s an option that should be used sparingly, because it can significantly extend the amount of time you’re in debt.”

How is my minimum payment calculated?

Each credit card company uses a different formula to calculate your minimum payment.

For some companies, your minimum payment is a percentage of your monthly balance, usually between 1% and 3% of your balance. In this case, you’re typically paying the same amount every month, regardless of your spending.

For other companies, your minimum payment is a fixed amount that also includes interest charges and fees, like making a late payment or exceeding your credit limit. In this case, your minimum payment can change a lot from month to month.

If your credit card balance is more than $1,000, your minimum payment will likely be a percentage of your total balance. If it’s less than $1,000, your minimum payment will likely a fixed amount, often $25. If your balance is less than $25, your minimum payment will likely be your total balance.

I’m convinced. Where do I start?

Start by figuring out how much you owe across all of your credit cards. Gather up all your statements and add up all your debt. Then, take note of every minimum payment amount and see how much more you can pay each month.

Remember to consider other debts and ongoing expenses. Making more than the minimum payment on your credit cards can affect other parts of your life. You may want to consider other ways to cut back on spending.

Whatever you do, be clear about your financial priorities. Avoid making a late credit card payment at all costs, even if it means only making the minimum payment one month. It’s important to stay on top of your credit card payments.

You can also look for ways to pay more than the minimum that work for your lifestyle, like collecting your spare change or making more meals at home. Every dollar counts, even if it’s a small amount. And if you ever get discouraged, stay focused on the future and making that final credit card payment.